Author

Corporate Health Outlook: Sentiment Cools, but Fundamentals Hold

The results from our latest survey of Loomis Sayles’ credit research analysts, known as the CANDIs, revealed that sentiment has taken a measured step back from more optimistic levels at the start of the year. Forward-looking sentiment cooled from elevated levels and several key indicators shifted in a less favorable direction. That said, the underlying credit story remains largely intact. Profit margins are holding at historically high levels, the risk of broad credit deterioration remains low and corporate balance sheets continue to look solid.

The geopolitical backdrop helps explain the shift. An extended conflict in the Middle East and associated oil price pressure have fed into cost expectations across a broad range of industries, tempering the optimism that characterized the first quarter. Reported earnings, however, have continued to exceed expectations, and we believe the fundamental case for credit remains supported by solid profitability and manageable debt levels.

About the CANDIs

Once a quarter, we survey Loomis Sayles’ credit research analysts to assess their bottom-up views of approximately 30 different industries. We quantify their responses using a proprietary tool known as the CANDIs—an acronym for Credit Analyst Diffusion Indices (click here to learn more). The process culminates in a forum that brings together our credit analysts and top-down global macro strategists to discuss the CANDIs’ output through the lens of the credit cycle. The results can be an indicator of how key corporate health metrics may trend over the next six months.

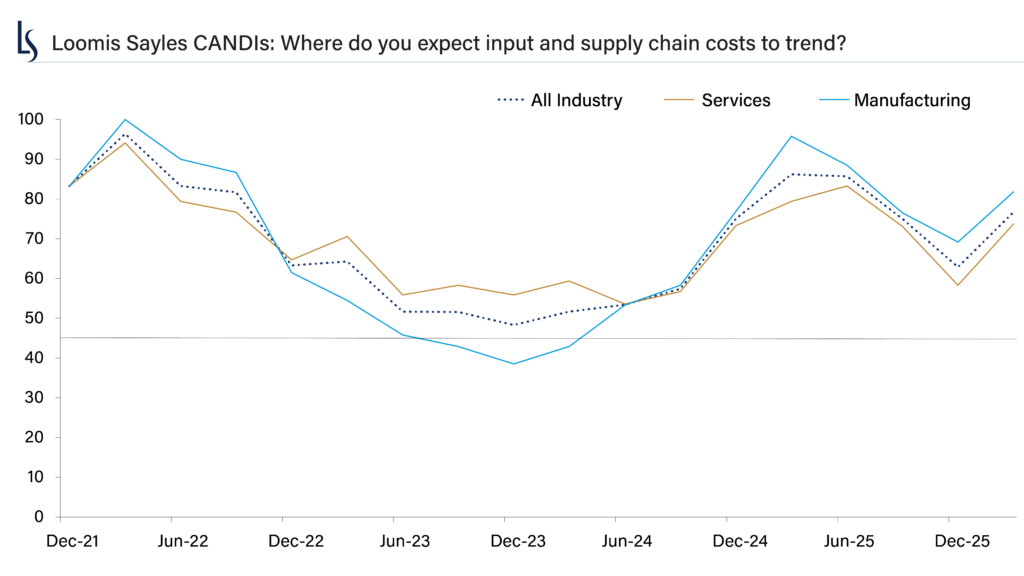

Costs resurge as the dominant pressure point

The sharpest move in the latest survey was in input and supply chain costs. Seventeen of thirty industries expect costs to move higher over the next six months. The increase was broad-based across both services and manufacturing, leaving few industries insulated from the pressure, with the combination of elevated oil prices and lingering tariff effects as the likely drivers.

Source: Loomis Sayles Credit Analyst Diffusion Indices, as of March 31, 2026. For the input and supply chain costs component, readings above 50 indicate a rising trend. The chart presented above is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization.

Leverage expectations also moved meaningfully higher, reversing much of the improvement seen in the January survey. Airlines, banks, building products and home construction were among the sectors expecting leverage to rise. Despite the uptick, overall levels remain manageable in our view.

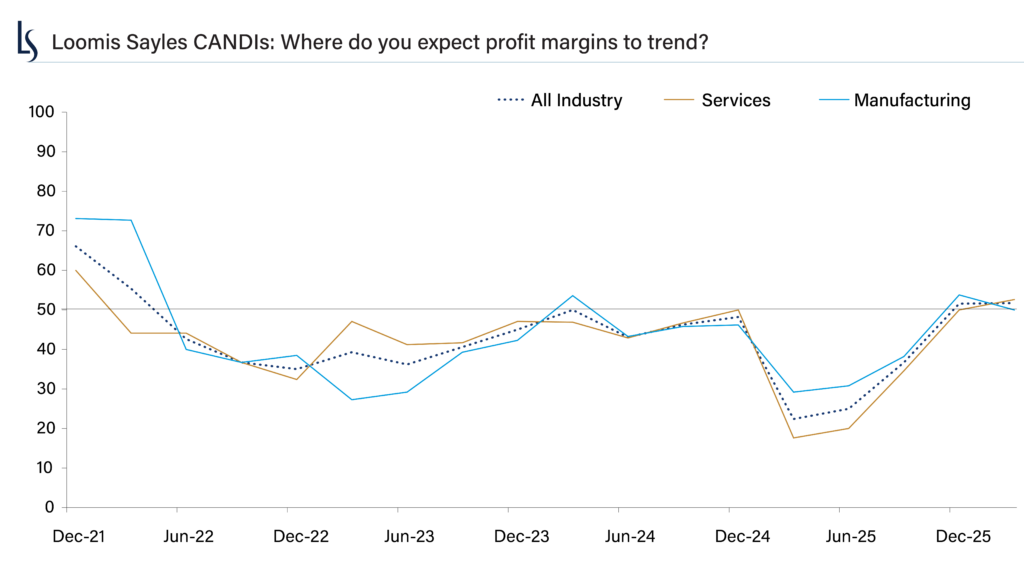

Margins hold; balance sheets remain the cycle’s anchor

We see the durability of profit margins as a reassuring signal. Margin expectations were essentially flat quarter over quarter, remaining in positive territory, which indicates that more analysts expect margins to expand than contract. S&P 500 Index profit margins stand at approximately 14%, a record level that companies have now defended for multiple consecutive quarters.i The CANDIs data is consistent with our view that margins can hold near these levels even if further expansion slows.

Source: Loomis Sayles Credit Analyst Diffusion Indices, as of March 31, 2026. For the profit margins component, readings above 50 indicate a rising trend. The chart presented above is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization.

However, companies will need to continue clearing a high bar to keep valuations supported, in our view. We also asked analysts whether artificial intelligence (AI) is affecting hiring intentions. The majority said “at the margin” or “not yet,” suggesting that any meaningful labor cost benefit from AI remains a forward-looking tailwind rather than a current support for margins.

Sentiment softens more than fundamentals

The credit outlook reading fell sharply, slipping below the neutral threshold for the first time since the middle of 2025. In the CANDIs framework, a reading below neutral means more analysts expect credit conditions in their industries to deteriorate than improve over the next six months. Manufacturing outlooks retreated particularly sharply from a positive to a neutral reading, while services fell below neutral. Consumer health remained the weakest reading in the survey and declined further, with service-oriented industries most exposed to value-conscious consumers and tighter household credit conditions.

We believe this softening in forward sentiment deserves attention, though context matters. Analyst outlooks can reflect both fundamental trajectory and external uncertainty, and the geopolitical backdrop appears to have weighed on the latter.

Carry is doing more of the work

The latest CANDIs results do not signal a fundamental break in the credit cycle, in our view. Corporate balance sheets remain solid and margins are holding at high levels. At the same time, forward momentum has moderated, and the gap between strong reported fundamentals and more cautious analyst sentiment is worth monitoring. While the expansion appears intact, it may be less forgiving than it was.

Credit spreads remain tight, reflecting the constructive fundamental backdrop that has characterized much of this cycle. But the rate environment has shifted. Higher yields have materially improved total return expectations, and we anticipate attractive six-month total return potential with carry across most US and non-US credit benchmarks. With meaningful spread compression unlikely from current levels, we believe potential opportunity lies in harvesting carry in a stable spread environment.

Endnote

i Source: Bloomberg, as of June 12, 2026.

8971102.1.1

Market conditions are extremely fluid and change frequently.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization. This information is subject to change at any time without notice

Meet the Author